*** UPDATE ***

Following the recent public health advice issued by the government, our Annual General Meeting and Special General Meeting scheduled to be held 26/03/2020 is postponed.

We will provide notice of the new proposed date for these meetings, following future guidance from the government.

On March 26th 2020 a Special General Meeting will be held to approve the following changes

1. Extend the credit union's common bond to cover Wakefield District Council

2. Amend the Rules of the Credit Union

See below the proposed rules of the credit union

1.0 Name

The name of this Credit Union shall be COMMUNITY FIRST CREDIT UNION LIMITED herein referred to as “the Credit Union”.

2.0 Registered Office

The Registered Office of the Credit Union shall be 1 MAIN STREET, MEXBOROUGH, SOUTH YORKSHIRE, S64 9LU or at such place as may from time to time be determined by the Board of Directors and registered with the relevant Authority.

3.0 Objects

The objectives of the Credit Union shall be:

4.0 Social Goals

The Credit Union may, by resolution of its Board of Directors, adopt one or both of the following additional social goals within its Policies:

5.0 Powers

The Credit Union shall have full power, subject to law, regulations and permissions granted to it by the Regulator, to do all things necessary or expedient for the accomplishment of its objectives.

6.0 Qualifications for and Admission to Membership

Admission to membership is restricted to those who fall within a common bond appropriate to a credit union, as follows:

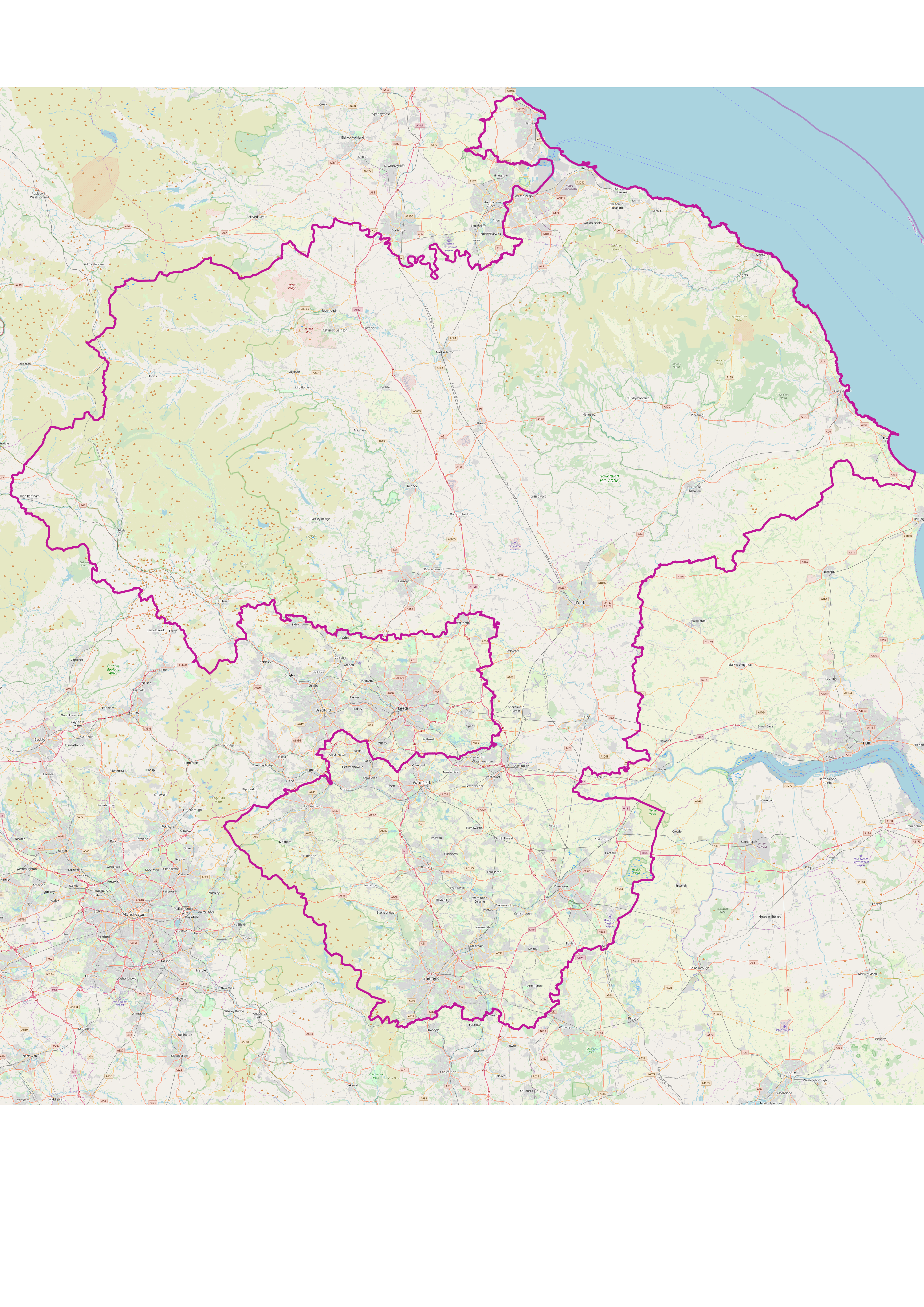

6.1 An individual who resides or is employed in the localities of:

Barnsley Metropolitan Borough Council

Doncaster Metropolitan Borough Council

Rotherham Metropolitan Borough Council

Kirklees Metropolitan Borough Council

York City Council

North Yorkshire County Council

Middlesbrough Borough Council

Redcar and Cleveland Borough Council

Hartlepool Borough Council

Sheffield City Council

Wakefield District Council

As delineated in red on the attached map, Rule 6.7 Common Bond.

6.2 A corporate body, individual in his/her capacity as a partner in partnership, an individual in his/her capacity as an officer or member of the governing body, if the body corporate, partnership or unincorporated association has:

6.3 An individual who is associated with other individuals through being a tenant of a social housing provider that administers property in the localities as delineated on the attached map.

6.4 An individual who is a member of the same household as, and is a relative of, an individual who is a member of the Credit Union and falls directly within a common bond specified above.

6.5 Subject to and in accordance with Rules 7 – 11 the membership of the Credit Union shall consist of individuals and bodies who have been admitted in accordance with Rule 6.

6.6 The minimum age of membership is eighteen (18) years. There is no maximum age limit, but life insurance benefits may be reduced or unavailable for older members.

6.7 Common Bond Map

7.0 Limitations on Membership

The Board of Directors shall ensure that at all times the number of Corporate Members in membership of the Credit Union does not exceed ten per cent (10%) (or other such amount as prescribed by law) of the total number of members of the Credit Union. If the number of Corporate Members should exceed the limit prescribed at any time, then the Board of Directors shall take all steps to reduce the number below the limit prescribed by expelling from membership those Corporate Members determined by the Board. In determining the policy for expulsion of Corporate Members the Board of Directors will conduct an assessment of the impact to the Credit Union of expelling any particular Corporate Member.

8.0 Joint Accounts

The Credit Union may offer a joint account facility to Members that are individuals. A joint account shall only be available to two (2) individuals who each qualify for, obtain and continue to hold membership under the common bond qualification. The Credit Union shall establish a procedure on the operation of the joint account.

9.0 Non Qualifying Members

9.1 An individual Member of the Credit Union who ceases to qualify for membership under Rule 6.1 may retain his or her membership and voting rights in the Credit Union and continue to acquire shares and receive loans. The membership, in a General Meeting, may set a limit on Non-Qualifying Members if it is deemed desirable.

9.2 The number of Non-Qualifying Members shall not exceed fifty per cent (50%) (or such other sum or limit as may be prescribed by law) of the total membership. If the number of Non-Qualifying Members shall exceed fifty per cent (50%) at any time then the Board of Directors shall take steps to reduce this number to below fifty per cent (50%). Ultimately the Board of Directors shall be required to expel from membership those who have most recently become Non-Qualifying Members, subject to these Rules.

10.0 Application for Membership

An Application for Membership may be admitted only when

a) It has been determined that the applicant fulfils the common bond for entry to

membership, Rule 6.1; and

b) The applicant has completed an application form; and

c) The applicant has provided sufficient evidence to prove his or her identity and address to comply with Money Laundering regulations and the law; and

d) The applicant has paid an entrance fee of an amount determined from time to time by the Board of Directors which fee shall be returned to the applicant if the application is refused; or has paid an annual fee of an amount that may be determined from time to time by the Board of Directors, and

e) The applicant has paid for at least one (1) share in the Credit Union.

11.0 Junior Savers

11.1 Children under the age of eighteen (18) (Junior Savers) may join the Credit Union if they are qualified for membership in accordance with Rule 6.1

11.2 Deposits from Junior Members must not exceed £10,000.00 or one point five per cent (1.5%) of total Non-Deferred Shares (or such other sum or limit as may be prescribed by law) in the Credit Union unless the deposits are held in a Child Trust Fund in which case the Credit Union can accept a larger deposit.

12.0 Cessation of Membership

A person shall cease to be a member of the Credit Union:

13.0 Withdrawal of Shares

Subject to Rule 20, a member may withdraw from membership at any time by applying for and receiving the shareholding in full in the Credit Union.

14.0 Expulsion from Membership

Subject to Rule 14 and 15 a member may be expelled from the Credit Union for any grave and sufficient reason including the following:

15.0 Appeal Against Expulsion

Where a member wishes to appeal against expulsion, the Board of Directors shall, upon written request of a member received not later than thirty (30) days after the date on which the notice has been served on him or her, convene an Appeals Sub-committee, appointed by the Board of Directors, to consider the matter of his or her expulsion. Such a member shall have the right to be represented and heard at such Appeals Sub-committee. The Appeals Sub-committee shall have the power, through a majority decision, to confirm the member’s expulsion or to direct that she/he shall remain a member of the Credit Union.

16.0 Liability of Members

17.0 Dormant Accounts

17.1 If a member has not:

17.2 The Credit Union shall not cancel or forfeit any member’s shares unless it has:

18.0 Shares

18.1 The Credit Union may issue Interest Bearing Shares if it meets the criteria for doing so as may be prescribed by law, the Relevant Authorities and these Rules, and shall be set and credited using a policy and procedure agreed by the Board of Directors .

18.2 When a member opens a share account, the Credit Union shall inform the Member whether the share account will qualify for interest or dividend as per these Rules. If a Member is informed they hold Interest Bearing Shares they must also be informed that if the Credit Union ceases to meet the criteria set out by law or the Relevant Authorities to pay interest on Shares, their Interest Bearing Shares will be converted to Dividend Bearing Shares. If a Member’s Interest Bearing Shares are converted to Dividend Bearing Shares, the member must be informed using an agreed policy and procedure by the Board of Directors.

19.0 Maximum Shareholding

19.1 No Member shall have, or claim an interest in, shares in the Credit Union, other than Deferred Share, exceeding the greater of £15,000.00 or one point five per cent (1.5%) of the total Non-Deferred Shares in the Credit Union (or such other sum or limit as may be prescribed by law). This rule applies to the sum of all accounts held by a member with the Credit Union. For the purpose of these rules the total shareholdings shall be that shown in the most recent audited balance to have been sent to the Regulator.

19.2 Corporate Members shall not have in total, or claim an interest in, fully paid up Non-Deferred Shares of the Credit Union exceeding twenty-five per cent (25%) (or such other amount as may be prescribed by law) of the total fully paid up Non-Deferred Shares of the Credit Union. If this percentage is exceeded, the Board of Directors shall repay Non-Deferred Shares held by Corporate Members using an agreed policy and procedure until the percentage is no longer exceeded.

19.3 The maximum Non-Deferred Shareholding limit of a joint account shall be double that of the limit on an account held by an individual. The amounts held in an individual account and joint account shall be amalgamated.

19.4 For the purpose of Rule 22 the total fully paid up Non-Deferred Shares in the Credit Union shall be taken to be the total fully paid up Non-Deferred Shares shown in the most recent annual return to have been sent to the Regulating Authority.

19.5 Shares in a Joint Account must not be held in the joint names of more than two (2) members. The interest of a member in a Joint Account shall be treated as fifty per cent (50%) of the shareholding in that account.

20.0 Withdrawing Shares

21.0 Insuring Shares

The Credit Union may enter into arrangements with a person carrying on the business of insurance for the purpose of providing insurance cover (for such sum or limit as may be prescribed by law) on the members of the Credit Union in relation to their shareholdings therein and any monies paid to the Credit Union by virtue of said insurance arrangements shall be credited to the share account of the insured member.

22.0 Interest on Shares

22.1 The Credit Union shall only pay different interest on different share accounts, where two-thirds of the members present in an Annual General Meeting or a Special General Meeting have agreed to offer interest bearing accounts; and the auditors are of the opinion that the Credit Union has maintained a satisfactory system of control and also has satisfactory systems of control in place to manage the payment of interest to members (for such sum or limit as may be prescribed by law or regulation).

22.2 The Credit Union shall not pay interest out of interim profits more than once a year.

22.3 The Credit Union shall only offer dividend bearing shares and interest bearing shares with the agreement of two-thirds of the members in an Annual General Meeting or a Special General Meeting. The Credit Union shall not offer interest bearing shares which also carry entitlement to a dividend, as this would result in a double payment.

23.0 Deferred Shares

23.1 Members of the Credit Union are eligible to purchase Deferred Shares which can be issued by the Credit Union and the terms and conditions shall be set out in the Issue Document. When a member purchases Deferred Shares they shall be issued with a share certificate denoting the ownership of the Deferred Shares.

23.2 The Credit Union must transfer an equivalent amount to reserves as a member has purchased Deferred Shares.

23.3 Deferred Shares are non-withdrawable but may be repaid or transferred only in the circumstances as set out in the issue document.

23.4 Members who hold both Non-Deferred Shares and Deferred Shares shall only have one (1) vote in the Credit Union.

24.0 Loans to Members

24.1 The Credit Union may make a loan to;

24.2 A loan shall not be made by the Credit Union to any member unless the loan is approved in accordance with the Credit Unions lending policy.

24.3 The Credit Union shall not at any time make a loan to a member if making such a loan would bring the total amount outstanding on a loan to members above such limits as may be set by law or by the regulators.

24.4 Both members of a joint account shall be held jointly and severally liable for the repayment of loans.

24.5 The Board of Directors shall determine from time to time the maximum amount that may, at a particular time, be on loan to a member either by way of secured loans or unsecured loans in accordance with rule 24.3.

24.6 The rate of interest chargeable on loans shall be determined from time to time by the Board of Directors , and shall not at any time exceed the rate of three per cent per month (or such other rate as may be prescribed by law or the Rules of the Regulating Authority) on the amount of the loan outstanding at the time and shall include all administrative charges and expenses incurred in making the loan.

24.7 Each application for a loan shall be submitted on a form provided by the Credit Union and shall state the purpose for which the loan is required, the security (if any) in respect thereof and such other information as may be required.

24.8 A Credit Union member may use his or her shares to guarantee another member’s loan, except that a member who is under eighteen (18) years of age may not act as a guarantor.

24.9 An Officer, Director or Employee of the Credit Union and their relatives may, if a member of the Credit Union, be granted a loan by the Credit Union in accordance with these rules, providing that;

24.10 The Credit Union shall not make a loan to an Officer, Director, Employee of the Credit Union and their relatives on terms more favourable than those available to other members of the Credit Union.

24.11 All applications for loans and loan registers shall be filed in accordance with the provisions of Rule 49.

24.12 The Credit Union may enter into arrangements with a person carrying on the business of insurance for the purpose of providing insurance cover on the liability of any member of the Credit Union.

24.13 Any person knowingly responsible for the issue of a loan to a person other than a member of the Credit Union shall be jointly and severally liable with the borrower to the Credit Union in the amount of the loan and accrued interest.

24.14 The Credit Union shall not lend for more than a period of time as set out in the Rules established by the Regulating Authority.

24.15 The Credit Union shall not lend to a member more than the amount as set out in the Rules or as established by the Regulating Authority.

24.16 The Credit Union shall make provision for bad or doubtful debts as set out in the Rules established by the Regulating Authority.

25.0 Recovering Loans from Members

25.1 The Board of Directors is responsible for ensuring that suitable policies and procedures are in place to ensure the repayment of all debts due to the Credit Union.

25.2 All sums due from any member shall be recoverable from him or her, his or her executors or administrators, as a debt due to the Credit Union.

25.3 The Credit Union shall have a lien on all shares of a member for any debt due to it by the member or for any debt that the member has guaranteed, and may set off any sum standing to the member’s credit including any shares, interest rebate and dividends, in or towards the payment of any debt.

26.0 Application of Surplus / Dividend

26.1 In ascertaining the profit and loss resulting from the operations of the Credit Union during any year of account, all operating expenses in that year shall be taken into account (including payment of interest) and provision be made for the depreciation of assets, tax liabilities and for bad and doubtful debts.

26.2 The Credit Union shall, out of its profits, each year maintain general reserves in accordance with the regulations.

26.3 The Credit Union may then allocate any remaining profits as follows:

26.4 A dividend on members’ dividend bearing shares may be recommended by the Board of Directors for declaration by the members at an Annual General Meeting. Such dividend shall be declared on all dividend bearing shares held during the previous financial year, a portion of a month being disregarded for the purpose of entitlement to dividend. No dividend declared and authorised for payment by the members in an Annual General Meeting shall exceed the rate recommended by the Board of Directors.

26.5 At each Annual General Meeting the members may be formally asked to delegate to the Board of Directors such powers as may be necessary to declare interim dividends and establish differential interest rates on different terms savings accounts. This delegation can only take place subject to regulatory restrictions placed on the operation of the Credit Union.

26.6 Provided that a dividend has been recommended by the Board of Directors in accordance with Rule 26 a rebate of interest, proportional to the interest paid or due from members during the year of account, may be recommended by the Board of Directors for declaration by the members at the Annual General Meeting. No rebate of interest declared and authorised for payment by the members in an Annual General Meeting shall exceed the rate recommended by the Board of Directors .

26.7 Dividends and interest rebates due to any member may be placed to the credit of his or her share balance and shall be so placed in any case where there is any money due from him or her to the Credit Union whether as a borrower, guarantor or otherwise in excess of his or her shareholding in the Credit Union, unless an application of such a dividend or interest rebate would increase his or her shareholding in the Credit Union to an amount exceeding the maximum shareholding permitted by Rule 19.

27.0 Investments

27.1 Subject to the general limitations as set out in the Rules established by the Regulating Authority the Credit Union may invest its surplus funds and funds serving liquidity.

27.2 All surplus funds not invested by the Credit Union, in accordance with Rule 27, must be held in cash in the custody of employees of the Credit Union

28.0 Borrowing

The Credit Union shall only borrow within the limits set out in the Rules of the Regulating Authority.

29.0 Capital

The Credit Union shall establish and maintain adequate financial resources in relation to its regulated activities as set out in the Rules of the Regulating Authority.

30.0 Liquidity

30.1 The Credit Union must at all times hold liquid assets of a value as set out in the Rules of the Regulating Authority.

30.2 The Credit Union shall maintain and implement an up-to-date liquidity management policy statement approved by the Board of Directors and complying with the Rules of the Regulating Authority.

31.0 Members Meetings

31.1 Meetings of the Credit Union shall be either Annual General Meetings or Special General Meetings. Every member holding at least one (1) share shall be entitled to attend such meetings on production of such evidence as the Board of Directors may from time to time determine.

31.2 At least twenty-one (21) days before the date of a meeting of members, the Board of Directors shall cause written notice of the date, time and venue by posting a notice in a conspicuous place in every office or place of business of the Credit Union where it may be read by the members, including any internet site operated by the Credit Union.

31.3 When notice of a meeting has been given in accordance with Rule 31, the accidental omission to give notice to any member thereof or the non-receipt of a notice by any member shall not invalidate any resolution passed or any proceedings taken at the meeting.

31.4 Ten per cent (10%) of the members of the Credit Union or fifteen (15) members, whichever is the lesser number, shall constitute a quorum for members meetings. A meeting may proceed to business if a quorum is present within half an hour after the time fixed for the commencement of the meeting. No meeting shall be incompetent to transact business for want of a quorum after the chair has been taken. If a special meeting convened on the requisition of members is inquorate then the meeting shall be abandoned.

31.5 Meetings called by the Board of Directors may, for good and sufficient reason, at the discretion of the chairperson, be adjourned.

31.6 The provision concerning notice, voting and quorum set in these rules shall apply to an adjourned meeting of members and no business shall be transacted at such a meeting other than business appearing on the agenda and left unfinished at the meeting at which the adjournment takes place.

31.7 If an Annual General Meeting or Special General Meeting convened by order of the Board or internal audit and compliance committee is inquorate, it shall stand adjourned to a later date within thirty (30) days, when the meeting so adjourned may proceed to business whatever is the number of members present.

32.0 Annual General Meetings

32.1 The Annual General Meeting shall be held within seven months of the end of the financial year at such date, time and place as the Board of Directors may by resolution decide.

32.2 The order of business at the Annual General Meeting of members shall be:

The members present at any Annual General Meeting may suspend or vary the order of business upon a majority of not less than two-thirds of the members present and voting at the meeting.

32.3 An Annual General Meeting may be made into a Special General Meeting for any purpose for which due notice has been given, provided that such business is not brought on until the business of the Annual General Meeting is concluded.

33.0 Special General Meetings

33.1 Any General meeting of the Credit Union other than an Annual General Meeting shall be a Special General Meeting. The Board of Directors of the Credit Union or the Internal Audit and Compliance Committee may for good and sufficient reason convene a Special General Meeting for any purpose not specifically provided for elsewhere in these Rules.

33.2 An Annual General Meeting may be made into a Special General meeting for any purpose of which due notice has been given under rule 32, providing that such business is not brought on until after the Annual General Meeting has been concluded.

33.3 The Financial Conduct Authority (FCA) may, on an application of at least ten percent (10%) of registered members, or (if less) one hundred (100) members;

a) appoint one or more inspectors to examine into and report on the credit unions affairs, or

b) call a special meeting of the credit union.

Further details on the process can be found on the FCA’s website.

33.4 A Special General Meeting shall not conduct any business not specified in the notice convening it.

34.0 Voting Rights and Procedure

34.1 Each member shall have one vote on each question at a meeting of the members of the Credit Union irrespective of his or her shareholding in the Credit Union. A member of the Credit Union may not vote by proxy at a general meeting of the Credit Union.

34.2 Votes at a general meeting of members shall be by show of hands, unless a secret ballot is requested by the Board of Directors or by ten (10) members present at the meeting. Subject to any special provisions contained in these rules or law, all resolutions shall be carried by a simple majority of votes cast.

34.3 Every meeting of members shall have a chairperson who shall, where the votes are equal, have an additional casting vote. The Chairperson of the Board of Directors shall, if present, take the chair at any meeting. If the chairperson is not present, the Vice-Chairperson shall do so, and if she/he is not present within fifteen (15) minutes of the stated start time of the meeting, the Board of Directors shall elect one of their number to do so.

35.0 Nominating Committee

35.1 The Board of Directors may appoint a Nominating Committee of not less than three (3) members of the Credit Union. The Nominating Committee shall ascertain the number of vacant positions requiring candidates and ensure there are sufficient candidates to recommend to the Annual General Meeting to fill all vacant positions.

35.2 The Nominating Committee shall ensure that any policy established by the Board of Directors regarding the suitability of candidates is adhered to.

35.3 The Nominating Committee shall also identify potential co-options to the Board of Directors to fill any vacancies.

36.0 Election Procedure

36.1 All elections shall be conducted following such procedure as may be established by the Board of Directors from time to time.

36.2 If there are outstanding vacancies, the chairperson of the meetings shall call for nominations from the floor. These, if duly proposed and seconded and if the nominee is present, or has given his or her consent in writing, shall be in order. All such nominates shall be members of the Credit Union.

36.3 If there are more candidates than vacancies (either by prior submission or by nomination from the floor) ballot papers shall be prepared listing the names of all candidates and each member present shall be allowed only as many votes as there are candidates.

36.4 The results of each election shall be announced by the chairperson. Candidates shall be placed in descending order of the number of votes cast for them and those candidates placed highest in the poll, equivalent to the number of vacancies to be filled shall be declared elected; providing that where there are more candidates nominated than the number of vacancies, no candidate shall be declared elected unless she/he has received votes from the majority of the members voting in the election. In the event of all vacancies not being filled in the first election, a further election or elections may be taken, the candidates for each election being all the remaining unelected nominees.

36.5 Notwithstanding the provision of Rule 36 if for any election the number of nominees does not exceed the number of vacancies to be filled, a motion to dispense with the election procedure and to declare elected all the nominees for that election may be proposed at the Annual General Meeting. If such a motion is carried by the majority vote of the members present at the meeting, the chairperson shall declare the nominees for election duly elected.

37.0 Suitability of Certain Persons to Hold Office

37.1 A person under eighteen (18) years of age may not be an officer or serve on the Board of Directors.

37.2 Where a person is, or becomes, an undischarged bankrupt or is, or has been, convicted on indictment of any offence involving fraud or dishonesty, the Board of Directors shall decide whether it is fit and proper to undertake responsibilities involved in the management of the Credit Union and whether to notify the Regulator. If the Board of Directors decides that the person is not fit and proper and/or the person is not approved by the Regulator, the person shall be prohibited from taking part in the running or management of the Credit Union.

37.3 When an employee of the Credit Union becomes an undischarged bankrupt or is convicted on indictment of any offence involving fraud or dishonesty, the Board of Directors shall require an investigation to be carried out and where required notify the Regulator. Depending on the findings of this investigation, disciplinary action may be taken which may result in dismissal.

38.0 Board of Directors and Sub-Committees

38.1 A minimum of one (1) weeks’ notice shall be given for meeting of the Board of Directors and sub-committees.

38.2 The number of members of the Board of Directors shall be not less than the legal minimum and the maximum number shall be determined from time to time by the members at a general meeting. Board Members (other than those appointed under Rule 38.6) shall be elected at the Annual General Meeting. The Board of Directors has the power to divide itself into a number of constituencies to ensure that the Board of Directors consists of representatives of all areas, sections and diverse groups covered by the Credit Union.

38.3 Members of the Board of Directors shall serve for a three (3) year term and retire at the third Annual General Meeting following their election. Retiring members of the Board of Directors shall be eligible for re-election.

38.4 Any Board Member who without due excuse accepted by the Board of Directors fails to attend three (3) consecutive board meetings shall, if the members of the board so resolve, be deemed to have vacated his or her office and the casual vacancy so created be filled as provided in Rule 38.

38.5 The office of a Board of Director shall be vacated if she/he:

38.6 A casual vacancy on the Board of Directors shall, as soon as practicable, be filled by a vote of the majority of the Board Members then holding office. Board Members so appointed shall hold office for the remainder of the unexpired term of office.

38.7 Regular meetings of the Board of Directors shall be held not less than once every month, the date, time and place to be decided by the Board of Directors.

38.8 A majority of the Board Members shall constitute a quorum for the transaction of business at any meeting of the Board.

38.9 Questions arising at any meeting of the Board of Directors shall be decided by a majority of votes. Each member shall have one vote on any matter and the chairperson of the meeting shall have a second or casting vote in the case of equality of votes.

38.10 The Board of Directors may delegate any of the powers hereby given to it to sub-committees consisting of such of their own number with such other members as they see fit.

38.11 The Board of Directors may also delegate any of the powers hereby given to it to officers in accordance with Rule 38.

38.12 Such sub-committees and officers shall, in the functions entrusted to them, conform in all respects to the instructions given to them by the Board of Directors.

38.13 The Board of Directors shall have the power to remove any committee and any officer and their respective powers and remunerations.

38.14 All acts done by any meeting of the Board of Directors or by any Board Member acting in pursuance of any authority duly given shall be valid, notwithstanding that it be afterwards discovered that there was some defect in the appointment or qualification of any Board Member that had been duly appointed or qualified.

38.15 No member of the Board of Directors of the Credit Union, other than the Treasurer or Assistant Treasurer, shall receive from the Credit Union remuneration, whether directly or indirectly, for any service performed by him or her in his or her capacity as such officer on behalf of or for the benefit of the Credit Union other than expenses necessarily incurred by him or her in such capacity in carrying out any duties in respect of the business of the Credit Union and approved by a majority vote of members of the Board of Directors.

38.16 Subject to law and these rules the Board of Directors shall have the general control, direction and management of the affairs, funds and records of the credit Union and more particularly shall:

38.17 Within the period of seven (7) days following the Annual General Meeting, the Board of Directors shall elect form its number a Chairperson, Vice-Chairperson, Treasurer and Secretary of the Credit Union and such other officers as are deemed necessary for the management of the Credit Union. A person so elected shall hold office until the election of his or her successor. Board Members undertaking a controlled function must be approved by the Regulator before they can perform such functions.

38.18 Subject to any specific provision contained in these rules the Chairperson, or in his or her absence, the Vice-Chairperson, shall preside at meetings of the Board of Directors and at meetings of members; she/he shall perform such other duties as she/he may be directed by the Board not inconsistent with the provision of law or these rules.

38.19 In the absence of both the Chairperson and the Vice-Chairperson, or neither is present within fifteen (15) minutes after the time appointed for the beginning of the meeting or if neither is willing to act, the members of the Board shall elect one of their number to be the chairperson of the meeting.

39.0 Credit Committee

39.1 The Board of Directors shall approve a loans policy that shall be applied equally to all members.

39.2 The Board of Directors may decide to establish a Credit and Loans Committee.

39.3 If the Board of Directors decide to establish a Credit Committee it shall consist of a minimum of three (3) committee members, elected by the Board of Directors within seven (7) days of the Annual General Meeting. The Credit Committee shall review the credit and loan policies of the Credit Union and may recommend changes to the policies to the Board of Directors .

40.0 Internal Audit Committee and Officers

40.1 In accordance with Rule 40 the Board of Directors shall establish an Internal Audit Committee consisting of Independent Supervisors who shall be elected by the Owner Members at the Annual General Meeting. Board members may not serve on the Internal Audit Committee.

40.2 The Internal Audit Committee shall choose from its number a Chairperson and Secretary. The Secretary shall maintain records of all actions taken by the Internal Audit Committee.

40.3 The Internal Audit Committee shall meet not less frequently than quarterly.

40.4 The Internal Audit Committee shall conduct independent checks of all credit union records to ensure that all policies, procedures and legislation are being adhered to, identify and correct errors, ensure early detection of fraud, improve the standards of the service to owner-members and ensure that the credit union is compliant.

40.5 Within a period of one (1) month following the Annual General Meeting, the Internal Audit Committee shall draw up a confidential audit plan for the following twelve (12) months.

40.6 Where the Internal Audit Committee has good and sufficient reason to believe the Credit Union may not be complying with the legislation, regulations, these rules and the Credit Union’s policies and procedures, or that financial records are not accurate and kept up to date or that fraud or theft may have occurred, the Internal Audit Committee shall report this to the Board of Directors, except in the case of suspicion of money laundering which is reported directly to the Money Laundering and Reporting Officer. If either no action is taken or the action fails to resolve the Internal Audit Committee’s concerns, the Internal Audit Committee shall convene a Special General Meeting of the owner-members under Rule 41. It shall also provide a written report to the Auditor, which shall include the date of the Special General Meeting of Owner Members who may by majority vote suspend from office the Board of Directors or any member thereof, provided, that no person shall be removed from office under this Rule without being given an opportunity to be heard or represented at such Special General Meeting of which he or she shall be given 14 days notice in writing.

40.7 To facilitate the work of the Internal Audit Committee, the Board of Directors may appoint or employ officer(s) to undertake internal audit duties and monitor compliance who shall not be a member of the Board of Directors of the Credit Union, to work under the direction and supervision of the Internal Audit Committee.

40.8 The officers undertaking internal audit duties shall keep a record of all work undertaken and shall provide a written report to the Internal Audit Committee not less than quarterly or as frequently as the Internal Audit Committee may prescribe.

40.9 Where an officer undertaking internal audit duties has good and sufficient reason to believe that the Credit Union may not be complying with the legislation, regulations, these rules or the Credit Union’s policies which govern its activities, or that financial records are not accurate and kept up to date or that fraud or theft may have occurred, he or she shall report this, in writing, to the Internal Audit Committee in the first instance. If either no action is taken or the action fails to resolve the officer’s concerns, he or she shall have the right to attend a meeting of the Board of Directors. If either no action is taken or the action fails to resolve the officer’s concerns, he or she shall provide a written report to the external Auditor.

40.10 If any Independent Supervisor or Supervisors on the Internal Audit Committee fail to carry out their duties correctly and in full then the Board of Directors if quorate in session and by a proposed, and seconded, motion can call a meeting of the Internal Audit Committee and can suspend them from duty, individually or in entirety, with justification also given in writing. When an Independent Supervisor/member of the Internal Audit Committee has been thus suspended from office and within seven days of suspension has not submitted his or her resignation, the Board of Directors shall convene for this purpose, a Special General Meeting of Owner Members, who may by majority vote suspend from office the Internal Audit Committee or any member thereof, that no person shall be removed from office under this Rule without being given an opportunity to be heard or represented at such Special General Meeting of which he or she shall be given 14 days notice in writing.

41.0 Secretary, Treasurer and Assistant-Treasurer

41.1 The Secretary shall give or cause to be given notice of all meetings of the members and the Board of Directors. She/he shall prepare and maintain minutes of all meetings and shall perform such other duties as the Board may from time to time determine.

41.2 The Treasurer shall, subject to such limitations and controls as may be imposed by the Board of Directors:

Posted: 03 March 2020